⚡ The Quick Answer

The IRS Tax Debt Help tool, launched April 16, 2026, lists six resolution options: payment plans, Offer in Compromise, collection delay (Currently Not Collectible status), penalty relief, innocent spouse relief, and special circumstances relief. It lists them accurately. What it does not do is qualify you for any of them, prepare the required documentation, or communicate with the IRS on your behalf. Each option has specific eligibility criteria, financial disclosure requirements, and processing timelines that the tool does not walk you through. Here is what each option actually takes to get approved.

When the IRS launched its Tax Debt Help tool on April 16, 2026, the coverage was largely positive. A free, anonymous tool that helps taxpayers understand their options without requiring a Social Security number or login is a genuine improvement over navigating irs.gov cold.

But reading a menu and ordering from it are different things. The tool points toward six resolution paths. Each of those paths has qualification criteria, documentation requirements, processing timelines, and failure rates that the tool does not describe. Knowing the name of an option is not the same as knowing whether you qualify, what the IRS needs from you to approve it, or what happens if the application is denied.

This guide covers each option the IRS tool lists, what the approval process actually involves, and where the gap between “the IRS offers this” and “you can get this approved” is large enough to warrant professional help. For a direct comparison of the tool versus hiring a tax relief firm, see our earlier guide on the IRS Tax Debt Help tool vs. hiring a tax relief company.

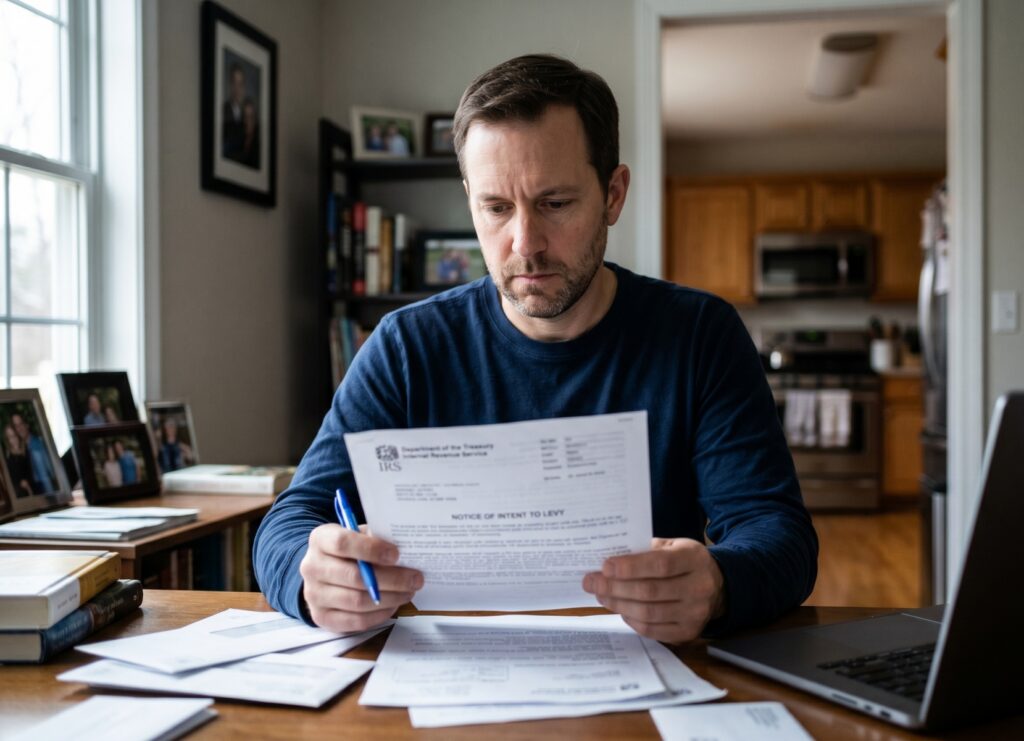

A Notice of Intent to Levy gives you 30 days to respond before the IRS begins seizing wages or bank accounts. Knowing which resolution option applies to your situation — and what it takes to get approved — is the difference between acting in time and missing the window.

The Six IRS Options: What the Tool Says vs. What Approval Requires

| Option | What the Tool Says | What Approval Actually Requires | DIY or Pro? |

|---|---|---|---|

| Payment Plan | Pay over time | All returns filed; debt under $50K for streamlined; Collection Information Statement for larger debts | DIY for under $50K |

| Offer in Compromise | Settle for less than you owe | Form 656, Form 433-A(OIC), full financial disclosure, $205 application fee, ~12 months processing | Pro recommended |

| Currently Not Collectible | Temporary delay if you can’t pay | Form 433-F or 433-A, full income/expense/asset disclosure, IRS agent review; debt does not go away | Pro recommended for complex cases |

| Penalty Relief | Request relief if you qualify | Form 843 or written request; must demonstrate reasonable cause, first-time abatement eligibility, or statutory exception | DIY possible; pro improves outcomes |

| Innocent Spouse Relief | Relief if affected by spouse’s debt | Form 8857, two-year deadline from first collection notice, IRS notifies ex-spouse, 6–12 month review | Pro strongly recommended |

| Special Circumstances | Disaster, military, identity theft | Varies significantly by program; most require separate applications and documentation | Case-by-case |

Option 1: Payment Plan (Installment Agreement)

What the IRS tool says: Pay over time with a short or long-term payment plan.

What approval actually requires: The IRS offers two tiers of installment agreements. The streamlined agreement covers taxpayers who owe $50,000 or less in combined tax, penalties, and interest and can pay within 72 months. It does not require a Collection Information Statement and can be set up online in minutes. This is the scenario where the IRS tool is genuinely sufficient for most people.

For debts above $50,000, the process changes materially. The IRS requires a completed Collection Information Statement (Form 433-A for individuals or Form 433-B for businesses), a detailed financial disclosure covering income, expenses, assets, and liabilities. The IRS uses this to determine what it considers your “ability to pay,” which may be higher than what you believe you can afford. Agents may challenge specific expense categories, require documentation for claimed expenses, and propose monthly payment amounts that create genuine hardship.

The IRS Fresh Start Program expanded installment agreement access and raised the streamlined threshold to $50,000. For a detailed breakdown of how that program works, see our guide to the IRS Fresh Start installment agreement.

The gap: For debt under $50,000 with all returns filed, the online application is straightforward and professional help is unlikely to change the outcome. For debt above $50,000, the Collection Information Statement negotiation is where professional representation materially affects the monthly payment amount you are locked into.

Option 2: Offer in Compromise

What the IRS tool says: Settle your tax debt for less than you owe, if you qualify.

What approval actually requires: The Offer in Compromise is the most misunderstood resolution option in the tax relief market, largely because it is the one most heavily marketed by companies promising dramatic results. The reality is more measured. The IRS accepted 13,176 OIC applications out of 36,033 submitted in the most recent reporting year, an acceptance rate of approximately 36%. The average accepted offer settled debt for roughly 20 cents on the dollar, but that figure reflects cases where the IRS determined the taxpayer genuinely could not pay more.

The application requires Form 656 (the formal offer), Form 433-A(OIC) (a comprehensive financial statement), a $205 non-refundable application fee, and an initial payment of either 20% of the offered amount (lump sum) or the first installment of a short-term payment plan. The IRS uses a specific formula based on your Reasonable Collection Potential (RCP) to evaluate whether your offer is acceptable. The RCP calculation includes your net equity in assets plus your projected future income over the collection period. If your offer falls below the IRS’s RCP calculation, it will be rejected.

Processing takes an average of 12 months. During that period, the statute of limitations on IRS collection is tolled (paused). If the offer is rejected, you have 30 days to appeal. A professional who understands the RCP calculation and knows how to document expenses and asset values appropriately can meaningfully affect whether an offer is accepted or rejected at a lower settlement amount. For a full walkthrough of the process, see our guide on how to get an Offer in Compromise approved.

The gap: The IRS tool links to the OIC Pre-Qualifier, which gives a rough eligibility estimate. It does not calculate your RCP, prepare Form 433-A(OIC), advise on how to value assets, or represent you if the offer is rejected. For a debt of $20,000 or more with a realistic path to OIC approval, professional representation is the highest-value use of tax relief fees.

Know Your Options. Then Get Help.

Compare Verified Tax Relief Companies

Our reviewed and ranked list covers firms that handle OIC, CNC, penalty abatement, and installment negotiations, with verified BBB standing and honest fee assessments.

Option 3: Currently Not Collectible (CNC) Status

What the IRS tool says: If you can’t pay now, you may qualify for a temporary delay.

What approval actually requires: Currently Not Collectible status is a formal IRS designation that temporarily halts all active collection activity: no levies, no wage garnishments, no bank seizures. It is granted when the IRS determines that collecting the debt would create genuine financial hardship based on your current income and necessary living expenses.

To obtain CNC status, you or your representative must submit a Collection Information Statement (Form 433-F for most individuals, or Form 433-A for more complex situations) demonstrating that your allowable monthly expenses equal or exceed your monthly income. The IRS uses its National Standards and Local Standards tables to determine which expenses it considers allowable, and these standardized amounts are often lower than actual costs in high-cost-of-living areas.

Two critical facts the tool does not emphasize: first, CNC status does not stop interest and penalties from accruing on the outstanding balance. The debt grows while collection is paused. Second, the IRS reviews CNC accounts periodically and will resume collection if your financial situation improves. The IRS typically identifies improvement through annual tax return data.

For a full breakdown of how CNC status works, the risks, and how to apply, see our guide on Currently Not Collectible status.

The gap: The IRS tool accurately describes CNC as a temporary delay. It does not explain how the IRS evaluates your Collection Information Statement, which expenses may be challenged, or how to document your financial position to maximize the likelihood of approval. For taxpayers with complex income sources or non-standard expense patterns, professional preparation of the 433-F significantly affects outcomes.

Option 4: Penalty Relief

What the IRS tool says: Request relief from penalties if you qualify.

What approval actually requires: IRS penalties can add 25% or more to your underlying tax debt and are often the fastest-growing component of a balance. Penalty relief is available through three distinct mechanisms, each with different eligibility criteria:

- First-Time Penalty Abatement (FTA): Available to taxpayers with a clean compliance history for the three years prior to the penalty year. The FTA is the most straightforward relief path and can be requested by phone or in writing without Form 843. The IRS does not advertise FTA aggressively, but it is available to any eligible taxpayer who asks.

- Reasonable Cause Abatement: Available when you can demonstrate that failure to pay or file was due to circumstances beyond your control, such as a serious illness, natural disaster, death of an immediate family member, or reliance on incorrect IRS advice. This requires a written statement and documentation. The IRS evaluates these requests case by case, and the standard is not lenient.

- Statutory Exception: Applies in narrow circumstances where the law specifically provides relief, such as certain disaster declarations or situations involving erroneous IRS written advice.

Penalty abatement is typically requested using Form 843 or a written explanation submitted with Form 843. Our guide to Form 843 instructions and IRS penalty relief covers the process step by step.

The gap: The IRS tool links to general penalty relief information. It does not identify which type of relief applies to your situation, help you determine whether you meet the three-year clean compliance requirement for FTA, or draft the reasonable cause argument that maximizes approval odds. First-Time Abatement is DIY-friendly for most people; reasonable cause arguments benefit from professional drafting.

Option 5: Innocent Spouse Relief

What the IRS tool says: Check if you qualify for relief if you’re affected by spousal debt or error.

What approval actually requires: Innocent Spouse Relief is one of the most procedurally complex options the IRS offers, and also one of the most time-sensitive. It protects a spouse or former spouse from liability for taxes, interest, and penalties resulting from the other spouse’s underreported income, erroneous deductions, or fraudulent filing.

There are three forms of innocent spouse relief: traditional innocent spouse relief (full relief from the other spouse’s errors), separation of liability relief (proportional allocation of the tax between spouses), and equitable relief (a catch-all for situations that do not qualify for the first two). Each has different eligibility criteria and different application standards.

The application is made on Form 8857 and must generally be filed within two years of the first IRS collection notice related to the joint liability. The IRS is required to notify the other spouse of the request, which can create legal and personal complications in divorce or separation situations. The review process typically takes six to twelve months.

For a full breakdown of who qualifies and how to apply, see our guide on innocent spouse relief and ex-spouse tax debt liability.

The gap: The two-year filing deadline is a hard cutoff that cannot be waived in most cases. Missing it permanently bars you from seeking relief on that liability. The legal and personal complexity of the process, combined with the strict deadline, makes this one of the options where professional representation is most clearly worth the cost.

Option 6: Special Circumstances Relief

What the IRS tool says: Check if you qualify for relief if you’re affected by a disaster area declaration, military deployment, or identity theft.

What approval actually requires: Each of these categories operates under its own rules.

Disaster relief is triggered by a federal disaster declaration and typically provides automatic extensions of filing and payment deadlines for affected taxpayers in the declared area. The relief is often automatic based on your address; you may not need to apply. Check irs.gov/newsroom/tax-relief-in-disaster-situations to confirm whether your area qualifies.

Military deployment relief extends deadlines for active duty personnel in combat zones and may provide interest and penalty waivers for the deployment period. The rules vary by branch of service and deployment type and are best verified directly with a military financial counselor or a tax professional familiar with servicemember tax law.

Identity theft relief applies when someone else filed a return using your Social Security number. The resolution process involves filing Form 14039 (Identity Theft Affidavit), working with the IRS Identity Protection Specialized Unit, and potentially waiting 12 to 18 months for the account to be corrected. This process is frustrating but largely procedural once the initial affidavit is filed.

The gap: The tool accurately points toward these categories. For disaster and military relief, the IRS process is often straightforward and self-directed. For identity theft, the resolution timeline is long but the steps are clear. Professional help is rarely necessary unless the identity theft has created complex multi-year filing complications.

What the Tool Does Not Cover at All

Beyond the gaps within each listed option, the IRS Tax Debt Help tool has no mechanism for two situations that frequently complicate real-world tax debt cases.

Unfiled returns. Every resolution option listed on the tool requires that all tax returns are filed. The tool notes this in a sidebar but does not walk you through the process of filing delinquent returns, which is often the prerequisite that must be completed before any resolution application can proceed. Tax relief companies routinely handle this as part of their engagement.

Active levies and garnishments. If the IRS has already issued a Notice of Levy or begun garnishing wages, the tool provides no mechanism for stopping or suspending those actions. A licensed representative with power of attorney can contact the IRS directly to request a Collection Hold while a resolution is being pursued. An anonymous online tool cannot.

When to Go Beyond the Tool: Verified Tax Relief Companies

The IRS tool is genuinely useful for taxpayers with straightforward situations. For everyone else, the following BestGuide-reviewed companies handle the full resolution process, including the documentation, negotiation, and IRS communication that the tool cannot perform. All have been evaluated on reputation, service range, pricing transparency, customer satisfaction, and outcomes.

Priority Tax Relief handles the full range of IRS resolution programs with licensed enrolled agents and CPAs. Strong fit for OIC and multi-year cases where comprehensive financial documentation is required.

Alleviate Tax is transparent on pricing at the outset of consultation and has earned strong client reviews for communication throughout long-running resolution cases.

Anthem Tax Services operates with attorney-backed case management and handles complex multi-year and business tax situations where the Collection Information Statement is the central negotiation point.

Five Star Tax Resolution offers direct attorney access and personalized case strategy, a strong fit for innocent spouse cases and situations requiring IRS appeals representation.

Tax Relief Advocates takes an aggressive negotiation posture and has a strong track record in penalty abatement and OIC cases where pushing back on the IRS’s initial position matters.

1099 Tax Problems specializes in self-employed and gig worker tax debt, including unfiled 1099 returns and self-employment tax liability, a niche that general-purpose firms often underserve.

Tax Group Center provides national coverage across federal and state tax issues with an in-house team of licensed professionals handling the full resolution spectrum.

Sources and Methodology

Resolution option details are sourced from the IRS Tax Debt Help tool (last reviewed April 13, 2026), IRS Publication 594 (The IRS Collection Process), IRS Publication 971 (Innocent Spouse Relief), and the IRS Offer in Compromise Booklet (Form 656-B). OIC acceptance rate data is from the most recent IRS Data Book. Company assessments follow BestGuide’s standard five-point evaluation methodology.

The Bottom Line

The IRS Tax Debt Help tool is an honest, useful orientation tool. It maps the territory accurately. What it cannot do is navigate it for you.

The practical summary by option:

- Payment plan under $50,000: The online application works. Handle it yourself.

- Payment plan over $50,000: Professional negotiation of the Collection Information Statement is worth the cost.

- Offer in Compromise: Use the OIC Pre-Qualifier to check rough eligibility, then hire a professional. The documentation and RCP calculation are where OICs are won or lost.

- Currently Not Collectible: Straightforward if your finances are simple. Complex income or expense situations benefit from professional 433-F preparation.

- First-Time Penalty Abatement: Call the IRS directly and request it. It is available to any eligible taxpayer who asks.

- Reasonable Cause Penalty Abatement: Professional drafting of the written argument meaningfully improves outcomes.

- Innocent Spouse Relief: Hire a professional. The two-year deadline is unforgiving and the process is legally complex.

- Disaster, military, identity theft: Follow the IRS-directed process for your specific situation. Professional help is rarely necessary unless complications have stacked up.

Ready to find a firm that handles your specific situation? See our full, reviewed ranking of best tax relief companies, with honest assessments of which firms excel at which resolution types.

Frequently Asked Questions

What options does the IRS Tax Debt Help tool cover?

The IRS Tax Debt Help tool, launched April 16, 2026, lists six resolution categories: installment agreements (payment plans), Offer in Compromise, collection delay (Currently Not Collectible status), penalty relief, innocent spouse relief, and special circumstances relief for disasters, military deployment, and identity theft. The tool accurately describes each option and links to IRS application pages, but does not evaluate your eligibility, prepare required forms, or represent you in the resolution process.

Can I get an Offer in Compromise without a tax professional?

Yes, the IRS accepts self-prepared OIC applications. However, the IRS accepted approximately 36% of OIC applications in the most recent reporting year. The primary determinant of acceptance is whether your offer meets the IRS’s Reasonable Collection Potential calculation, which requires accurate valuation of assets and projected future income. Tax professionals familiar with OIC preparation understand how to document expenses and asset values in ways that align with IRS standards, which materially affects acceptance rates for qualifying cases.

What is First-Time Penalty Abatement and how do I get it?

First-Time Abatement (FTA) is an IRS administrative waiver available to taxpayers with a clean compliance history for the three years prior to the penalty year. It can be requested by calling the IRS directly at (800) 829-1040 or in writing, without requiring Form 843. The IRS does not proactively offer FTA; you must request it. Eligible taxpayers who request FTA by phone typically receive a decision on the call. See our Form 843 and penalty relief guide for the full process.

What happens if the IRS denies my Offer in Compromise?

If the IRS rejects your OIC, you have 30 days from the date on the rejection letter to file an appeal with the IRS Office of Appeals. The appeal must explain why you disagree with the IRS’s determination and can include additional financial documentation. If the appeal is also unsuccessful, you can refile a new OIC if your financial circumstances have changed, or pursue an alternative resolution path such as an installment agreement or Currently Not Collectible status. A tax professional can advise on the strongest path after a rejection.

1099 Tax Problems

1099 Tax Problems Alleviate Tax

Alleviate Tax Anthem Tax Services

Anthem Tax Services Priority Tax Relief

Priority Tax Relief Tax Relief Advocates

Tax Relief Advocates