⚡ Key Takeaways

- The Servicemembers Civil Relief Act (SCRA) caps interest at 6% on pre-service debt during active duty, including credit cards, auto loans, mortgages, and most student loans.

- The Military Lending Act (MLA) limits the Military Annual Percentage Rate to 36% on consumer credit taken on during service, with no mandatory arbitration and no prepayment penalty.

- The Department of Veterans Affairs handles only VA-related debts, such as benefit overpayments and copay bills. Credit cards, personal loans, and private medical debt fall outside that scope.

- For non-VA debt, veterans choose between settlement, consolidation, nonprofit credit counseling, and bankruptcy. Each path has a different cost, credit impact, and eligibility profile.

- The HAVEN Act excludes most VA disability and similar benefits from the Chapter 7 means test, restoring bankruptcy access to many disabled veterans who were previously priced out.

Why veteran debt needs its own playbook

Veterans carry more consumer debt than civilians on average, and they reach those balances by a different route. Frequent moves, deployment-related income shocks, and the transition to civilian employment compress the timelines that normally smooth financial decisions. The result is visible in the numbers. Survey data compiled by the American Consumer Credit Counseling shows roughly 91% of military families hold at least one credit card, and 27% carry $10,000 or more in card debt, compared with 16% of civilian households.

The other piece of context is professional. A weak credit profile can affect security-clearance reviews, reenlistment eligibility, and certain housing decisions, so debt is not only a financial problem for service members and recent veterans. That overlap is why federal law gives military borrowers protections civilians do not have, and why the playbook for veteran debt relief looks different from the one in our general guide on what debt relief actually is and how it works.

Federal protections built for military service

Two federal statutes set the baseline. The Servicemembers Civil Relief Act (SCRA) covers debts you took on before active duty. The Military Lending Act (MLA) covers debts you take on during active duty. Together, they touch most of the credit a service member will encounter, and both are enforced by the Consumer Financial Protection Bureau (CFPB) and the Department of Justice (DOJ).

SCRA: a 6% cap on pre-service debt

The Servicemembers Civil Relief Act caps interest at 6% on auto loans, mortgages, credit cards, other installment loans, and student loans originated after August 14, 2008, provided the obligation predates active duty. The protection runs throughout active duty for most debts and extends one year past your last day of active service for mortgages. Interest above 6% is forgiven during that window, not deferred for later collection.

The cap is not automatic. You must submit a written request to each creditor with a copy of your military orders, and you have up to 180 days after the end of active service to do so. CFPB enforcement data on Guard and Reserve members suggests the benefit is widely underused. The agency estimates fewer than 10% of eligible auto loans and 6% of eligible personal loans actually receive the SCRA reduction, a gap the joint DOJ-CFPB enforcement letter issued in December 2024 was designed to close.

MLA: a 36% MAPR ceiling on consumer credit

The Military Lending Act caps the Military Annual Percentage Rate at 36% on most consumer credit extended to active-duty service members and their dependents. The MAPR is broader than the standard APR. It includes credit-insurance premiums, debt-cancellation product fees, and most application and participation fees, which means lenders cannot inflate the effective rate through ancillary charges.

The MLA also bars mandatory arbitration, voluntary allotments tied to loan approval, prepayment penalties, and contractual waivers of SCRA rights. Residential mortgages and motor-vehicle purchase loans secured by the vehicle being financed are the main exclusions. If you are on active duty and a lender quotes anything above a 36% MAPR on a covered product, the underlying contract is void from inception under federal regulation.

VA debt help: when the agency steps in, and when it doesn’t

The Department of Veterans Affairs is not a general-purpose debt-relief agency. VA debt management programs apply only to debts you owe directly to the VA. The most common categories are benefit overpayments from a disability-rating change, copay charges from VA health care, and recoupment of education benefits like GI Bill funds. Credit-card balances, personal loans, private medical bills, and auto loans fall outside that scope.

Within VA debt itself, four tools are available. You can request a repayment plan, file a Financial Status Report (VA Form 5655) to ask for a waiver, propose a compromise offer for a one-time reduced payment, or apply for a temporary hardship suspension that pauses collection while you stabilize your finances. The application window for a waiver is one year from the date of the first debt letter, and acting within the first 30 days of a bill avoids late fees and interest.

One overlap is worth flagging. If you own a home with equity, a VA-backed cash-out refinance can pay off unsecured balances at mortgage rates rather than credit-card rates. The mechanism is a mortgage product, not a debt-relief program, but it functions as one for veteran homeowners. We cover the mechanics, eligibility, and trade-offs in our dedicated guide to the VA debt consolidation loan.

General debt relief options for veterans

Outside the SCRA, MLA, and VA-specific tools, veterans use the same four paths available to civilians. Each path solves a different problem, and the right fit depends on the type of debt, the amount, and the borrower’s income stability.

Debt settlement

Debt settlement negotiates a lump-sum payoff for less than the full balance, typically on unsecured debt above $10,000. The mechanics work the same way for service members and civilians. Programs run 24 to 48 months, fees fall between 15% and 25% of enrolled debt, and credit scores typically drop 65 to 125 points before recovering. Our National Debt Relief review walks through how the company structures veteran enrollments, including its handling of pre-service debt that may already qualify for an SCRA reduction. The Federal Trade Commission bans upfront fees, so any provider asking for payment before settling at least one account is operating outside federal rules.

Debt consolidation

Consolidation combines multiple balances into one loan, ideally at a lower rate. Veterans have access to civilian personal loans, balance-transfer credit cards, and the category-specific VA cash-out refinance for homeowners. Consolidation works when the new rate is meaningfully lower than the weighted average of the old debts and when the borrower can sustain on-time payments through the new schedule. For a head-to-head comparison of consolidation against the other main path, see our pillar on debt consolidation vs. debt settlement.

Nonprofit credit counseling and DMPs

A nonprofit credit-counseling agency can build a debt management plan (DMP) that consolidates payments to creditors and negotiates lower interest rates without a new loan. Setup fees are typically $30 to $50, with monthly maintenance fees of $25 to $75. DMPs run 36 to 60 months. The trade-off is that most plans require closing the enrolled credit accounts during the repayment period, which compresses available credit while the plan runs.

Bankruptcy with HAVEN Act protections

For veterans whose debt is genuinely unaffordable, bankruptcy is the benchmark the other options should be measured against. The Honoring American Veterans in Extreme Need (HAVEN) Act, passed in August 2019, excludes most VA and Department of Defense disability and similar benefits from the Chapter 7 means test, the income calculation that determines Chapter 7 eligibility. Disabled veterans with a 30% or higher service-connected disability rating may also qualify for a means-test exemption when their debts were incurred during active duty.

If you suspect your debt is unmanageable and your income is constrained, a consultation with a bankruptcy attorney is the right diagnostic step. You can use AttorneyReview’s directory to find a bankruptcy attorney in your state, including practitioners who handle SCRA, HAVEN Act, and military-specific bankruptcy issues.

Programs at a glance: who qualifies and what each one solves

The table below puts the veteran-specific protections next to the general debt-relief tools so the trade-offs are visible in one frame.

| Program | Who Qualifies | What It Solves | Cap or Typical Cost |

|---|---|---|---|

| SCRA interest rate cap | Active-duty members with pre-service debt | High-rate pre-service auto, mortgage, credit card, and student loan debt | 6% APR cap during active duty (mortgages: +1 year) |

| Military Lending Act | Active-duty members and dependents | High-cost consumer credit taken on during service | 36% MAPR cap, all-in |

| VA cash-out refinance | Veterans with VA loan eligibility and home equity | Consolidating unsecured debt into a VA-backed mortgage | Up to 100% LTV (lender-dependent) |

| VA debt waiver or compromise | Veterans with VA-only debts (overpayments, copays) | Forgiving or reducing VA-related balances | Filed via VA Form 5655 within 1 year |

| Debt settlement | Veterans with $10,000+ in unsecured debt and hardship | Credit cards, personal loans, medical bills | 15%–25% fee on enrolled debt |

| Nonprofit DMP | Veterans with steady income and unsecured debt | Lowering rates and consolidating payments without a new loan | $30–$50 setup + $25–$75 monthly |

| Chapter 7 bankruptcy (HAVEN Act) | Veterans whose excluded benefits clear the means test | Discharging unsecured debt within roughly 4–6 months | $338 court fee + $1,000–$3,500 attorney |

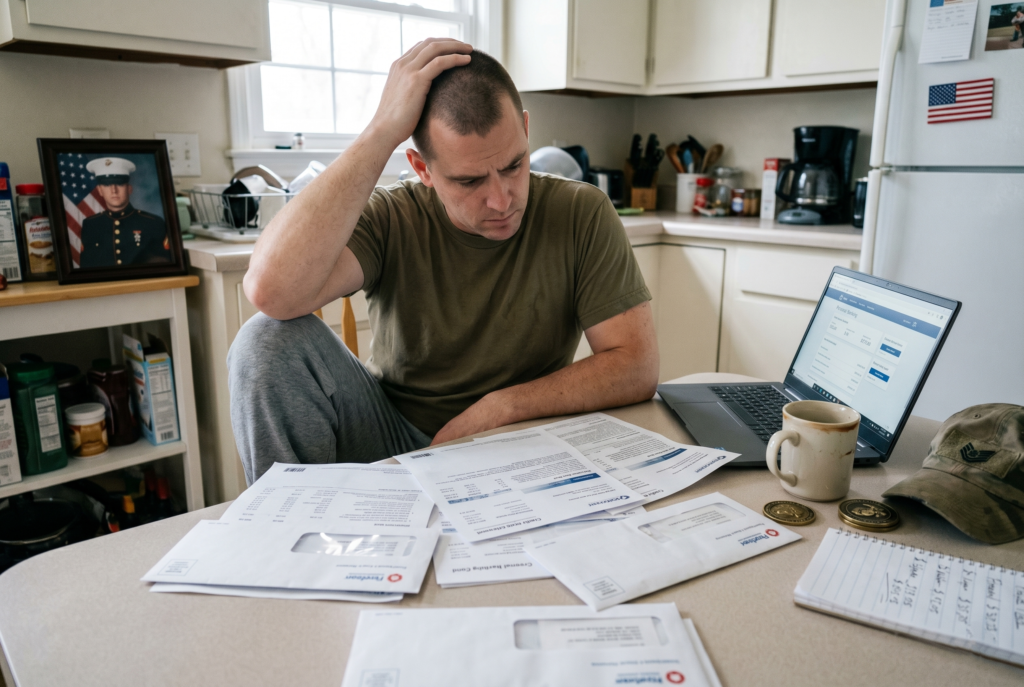

A Marine Corps veteran reviews credit card statements and a banking dashboard at his kitchen table. For most veterans, this is where the debt relief decision actually starts, before any SCRA filing, VA refinance, or settlement program enters the picture.

Compare Options

Find a Debt Relief Company That Works With Veterans

Side-by-side fees, BBB ratings, program timelines, and AFCC accreditation across the providers we cover.

How to choose the right option for your situation

The right path depends less on a general preference and more on three variables: the type of debt, the amount, and your monthly cash position. The three profiles below cover the scenarios we see most often in this category.

Active-duty service member with pre-service debt

Start with SCRA enforcement. Submit a written 6% rate-reduction request to every creditor that holds covered pre-service debt, with a copy of your orders, before considering any settlement or consolidation product. A balance carried at 22% APR drops to 6% the moment the request is properly filed, and the difference is forgiven for the active-duty period. Once the cap is in place, evaluate remaining post-cap balances against MLA-compliant consolidation products before any settlement enrollment.

Veteran with consumer debt and home equity

Compare a VA cash-out refinance against debt settlement. Refinancing pulls equity to retire unsecured balances at mortgage rates, which is almost always cheaper than 15%–25% settlement fees on the same balances. The trade-off is that you convert unsecured debt into secured debt against your home. Our Freedom Debt Relief review shows how a settlement quote is typically structured for this profile, which makes the cost comparison cleaner. Credit Saint’s guide on credit repair versus debt consolidation covers the credit-score side of the same decision.

Veteran with overwhelming debt and constrained income

Run the bankruptcy means test with HAVEN Act exclusions before signing onto a 48-month settlement program. If your VA disability and similar benefits are excluded from the income calculation, Chapter 7 may discharge unsecured balances in 4 to 6 months rather than 4 years, at lower total cost. Talk to a bankruptcy attorney who handles HAVEN Act cases before assuming Chapter 7 is closed to you because of VA income.

The decision a veteran should make on debt relief

The framework that fits most veterans is to exhaust the no-cost protections first, then choose among paid options by total cost rather than monthly payment. SCRA and MLA enforcement are free. VA hardship tools are free. Once those are in motion, the right paid option is the one that closes the debt at the lowest total cost given your timeline, your tax exposure on forgiven debt, and the credit-recovery window you need before your next major borrowing event. Settlement is rarely the cheapest path for a veteran homeowner with equity. Bankruptcy is rarely worse than a 4-year settlement program for a veteran whose income relies primarily on VA disability benefits. Run both math problems before signing anything.

Recommended

Considering Consolidation? Read This First.

Our full breakdown of VA-backed consolidation loans covers eligibility, rates, and how they compare to debt settlement for veterans.

Frequently asked questions

Does the VA forgive credit card debt?

No. The VA’s debt programs cover only debts owed to the VA directly, such as benefit overpayments and copay charges. Credit cards, personal loans, and medical bills from private providers fall outside the agency’s scope and are addressed through civilian options like settlement, consolidation, credit counseling, or bankruptcy.

How does the SCRA’s 6% interest rate cap work?

The Servicemembers Civil Relief Act caps interest at 6% on debts taken on before active duty, including credit cards, auto loans, mortgages, and post-2008 student loans. You activate the cap by submitting written notice to each creditor with a copy of your military orders, no later than 180 days after the end of active duty. Interest above 6% is forgiven during the protected period, not deferred for later collection.

Can a veteran qualify for debt consolidation with bad credit?

Yes, but options narrow as the score drops. Veterans with a credit score above 640 typically qualify for unsecured consolidation loans. Below that, the practical options are a VA cash-out refinance for homeowners, a secured personal loan, or a debt management plan through a nonprofit counselor, which does not require a credit-based approval. Debt settlement does not require a minimum credit score, but it is structured around hardship and damages credit further during the program.

Does filing for bankruptcy affect my security clearance?

Filing for bankruptcy is generally not, by itself, a disqualifier for a security clearance. Adjudicators look at the pattern of financial behavior and the cause of the debt. A bankruptcy filed in response to deployment, medical hardship, or divorce is treated very differently from one driven by gambling, fraud, or undisclosed liabilities. Disclosing the filing proactively to your security officer is the standard practice.

Is there a special debt relief program just for veterans?

No federally administered debt-forgiveness program exists exclusively for veterans on consumer debts like credit cards or medical bills. Ads that promise a “Veterans Credit Card Forgiveness Program” or guaranteed military debt elimination are scams, and the Federal Trade Commission has flagged them repeatedly. The actual veteran-specific tools are SCRA rate protections, MLA lender restrictions, VA-internal debt relief on VA debts, and HAVEN Act bankruptcy treatment.

Cambridge Credit Counseling

Cambridge Credit Counseling Debt Relief Advocates

Debt Relief Advocates