⚡ The Quick Answer

As of July 7, 2026, the best CD rates reach about 4.94% APY on select shorter terms, roughly double the national average for a 1-year certificate. With the latest inflation reading at 4.2%, a 4.94% APY still edges out rising prices, though the real return is slim. The Federal Reserve held its benchmark rate steady in June, so locking a competitive rate now removes the guesswork about where yields head next. Compare the APY, term, early withdrawal penalty, and federal insurance status before you commit.

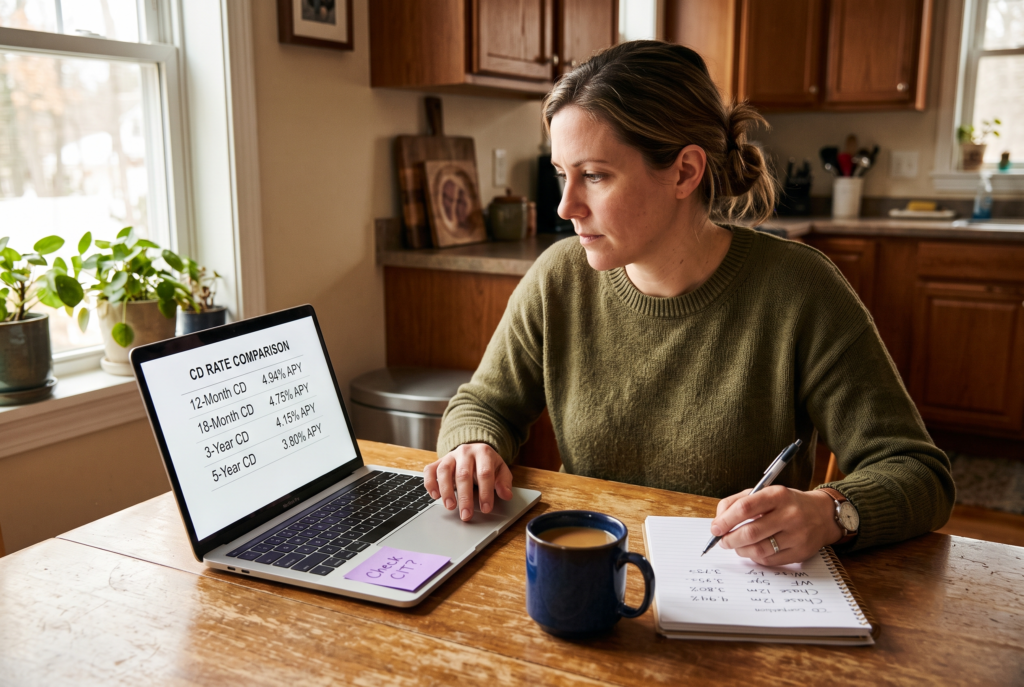

Where CD rates stand in July 2026

Today’s landscape still offers meaningful opportunity even as yields drift below their 2024 peaks. The national average for a 1-year CD sits near 2.00% APY, and the FDIC’s official national rate runs lower still, yet top online banks and credit unions pay well above both. Leading rates reach as high as 4.94% APY on shorter terms, and online banks like Marcus by Goldman Sachs and Bask Bank routinely top the national average by a wide margin. That gap is exactly why it pays to shop around.

The Federal Reserve held the federal funds rate steady at its June 2026 meeting, keeping the target range at 3.50% to 3.75%. When the Fed pauses, CD rate movement tends to flatten. Locking a rate today removes the uncertainty of where yields will sit three or six months from now.

What 4.94% APY actually means for your savings

Annual percentage yield, or APY, reflects the total return you earn in a year including compound interest. A $10,000 deposit in a 12-month CD at 4.94% APY generates roughly $494 in interest after one year, assuming you leave the principal and interest untouched. That is more than double what the same deposit would earn at the national average.

That return is nominal, meaning it is not adjusted for taxes or inflation. With the Consumer Price Index up 4.2% year over year in the latest reading from the Bureau of Labor Statistics, a 4.94% APY delivers a positive real return of roughly 0.7 percentage points. That spread is slim, and it narrowed as inflation ticked up from 3.8% the prior month, but it still preserves purchasing power in a way that most standard savings accounts do not.

How CD terms shape the rates you see

The highest advertised rates today often cluster in the 6-month to 18-month range. A 6-month CD may show 4.94% APY while a 5-year CD from the same institution offers closer to 3.80% APY. This inverted relationship, where shorter terms pay more than longer ones, reflects market expectations that rates will decline over time.

Choosing a term is a trade-off. Shorter terms capture today’s high rate but expose you to reinvestment risk when the CD matures. Longer terms lock a rate for years, which helps if rates fall, but they carry steeper early withdrawal penalties. The Consumer Financial Protection Bureau notes that a 5-year CD penalty often equals six to twelve months of interest, which can erase a large share of your earnings if you need the money early.

Comparing CD rates across terms is the fastest way to see where today’s best APY sits before you lock in.

Federal insurance and the safety of your principal

Certificates of deposit are among the lowest-risk places to hold cash, provided the issuing institution carries deposit insurance. FDIC coverage protects up to $250,000 per depositor, per insured bank, for each account ownership category. Credit unions offer equivalent protection through the National Credit Union Administration, or NCUA. Verify an institution’s status on the FDIC BankFind tool or the NCUA credit union locator before opening an account.

One caveat: brokered CDs, which you buy through a brokerage account, carry different liquidity risks than bank-issued CDs. They typically offer FDIC insurance on the underlying deposit, but selling a brokered CD before maturity on the secondary market can produce a loss if rates have risen since purchase. The fixed principal protection applies only if you hold to maturity.

Why early withdrawal penalties deserve a close look

Every CD comes with an early withdrawal penalty, and the structure varies widely. A 1-year CD penalty might equal 90 days of simple interest, while a 3-year CD penalty could equal 180 days. Some institutions calculate the penalty on the full balance including accrued interest, while others limit it to the original principal. Before you fund a CD, ask the institution for a dollar-amount example of the penalty on a $10,000 deposit, because seeing the actual number makes the trade-off concrete.

There is no federal cap on early withdrawal penalties. Reading the Truth in Savings disclosure, which banks are required to provide under federal law, is the most direct way to confirm the exact terms before you sign.

A framework for comparing CD offers

Use a consistent set of criteria when you evaluate providers. The table below outlines what to check before committing funds, and you can compare CD rates across banks side by side to speed up the process.

| Factor | What to look for |

|---|---|

| APY | The advertised rate versus the national average for that term. Confirm it is not a teaser rate that drops after an introductory period. |

| Term length | Match the term to a specific goal. A 6-month CD suits a near-term expense; a 3-year CD fits a medium-term goal. |

| Minimum deposit | Some top-rate CDs require $1,000 or more; others have no minimum. Know the threshold before you apply. |

| Early withdrawal penalty | Expressed in days or months of interest. Calculate the dollar cost on your actual deposit amount. |

| Insurance status | FDIC or NCUA coverage, verified through the agency’s public database. |

| Compounding frequency | Daily or monthly compounding lifts the effective yield slightly. APY already accounts for this, so compare using APY. |

Using a CD ladder to manage rate uncertainty

A CD ladder splits your total deposit across multiple terms, such as 6, 12, 18, and 24 months. As each rung matures, you reinvest the proceeds at the prevailing rate. This reduces the risk of locking all your money at a rate that looks unattractive a year from now, while still capturing today’s elevated short-term yields.

For example, with $20,000 you might place $5,000 in a 6-month CD at 4.94% APY, $5,000 in a 12-month CD at 4.15% APY, $5,000 in an 18-month CD at 4.05% APY, and $5,000 in a 2-year CD at 4.00% APY. When the 6-month rung matures, you reinvest it in a fresh 2-year CD, keeping the ladder rolling. A ladder is a common way to balance liquidity and yield when the rate path is uncertain, and building one across a few well-rated banks like Capital One Bank is straightforward.

Tax implications of CD interest

Interest earned on CDs is taxable as ordinary income at the federal level, and your institution issues a Form 1099-INT if you earn $10 or more in interest during the tax year. The IRS requires you to report this income even if you do not withdraw the interest. For a $10,000 CD earning $494 in a year, a taxpayer in the 22% federal bracket would owe roughly $109 in federal income tax on that interest.

State income tax may also apply, depending on where you live. If you hold CDs inside a tax-advantaged account such as an IRA, the interest grows tax-deferred or tax-free, depending on the account type. Early withdrawals from an IRA CD can carry additional tax consequences, so consult a qualified tax professional before structuring retirement-account CDs.

When a CD makes sense, and when it does not

A CD is a strong fit for money you will not need until a known date. An emergency fund, by contrast, belongs in a liquid account where you can reach the cash instantly without penalty. The guideline we follow: if the expense is less than six months away, a high-yield savings account or money market fund usually provides enough yield with full liquidity. You can weigh the two side by side with our high-yield savings account comparison.

The genuine limitation of a CD is its rigidity. If an unexpected expense arises, the penalty can more than offset the higher rate you earned relative to a savings account. For savers who value flexibility over the last few basis points of yield, a no-penalty CD is worth a look. No-penalty CDs pay slightly lower rates but let you withdraw the full balance after a short holding period without forfeiting interest.

Bottom line: how to decide

Match the term to a dated goal, then pick the highest APY from a federally insured bank whose early withdrawal penalty you have priced out in dollars. If your timeline is fuzzy or under six months, keep the cash liquid instead. If it is fixed and six to eighteen months out, today’s 4.94% APY is a rate worth locking, and a ladder lets you capture it without committing every dollar to one term.

- Top CD rates reached about 4.94% APY as of July 7, 2026, just ahead of the 4.2% inflation rate reported by the Bureau of Labor Statistics.

- The national average 1-year CD sits near 2.00% APY, so compare online banks and credit unions rather than accepting the rate at a single institution.

- Verify FDIC or NCUA insurance through the agency’s public lookup tool before depositing funds.

- Calculate the dollar cost of the early withdrawal penalty on your deposit; a high APY can be wiped out by a steep penalty if you need the money early.

- Match the term to a goal, and consider a CD ladder to balance rate capture with liquidity.

- CD interest is taxable as ordinary income, so factor the after-tax return into your decision.

Frequently asked questions

Are CD rates expected to go up or down in 2026?

No one can predict future rates with certainty. The Federal Reserve held rates steady at its June 2026 meeting, and with inflation still running above the Fed’s 2% goal, the near-term path is uncertain. Locking a rate now removes that uncertainty for the term you choose.

What is the difference between APY and the interest rate on a CD?

The interest rate is the nominal rate the bank pays on your deposit. APY reflects the total return including compound interest over a full year. Always compare APY, not the base rate, because it accounts for how often interest compounds.

Can I lose money in a CD?

If you hold a bank-issued CD to maturity and the institution is FDIC or NCUA insured, your principal is protected up to the insurance limit. You can lose money if you withdraw early and the penalty exceeds the interest earned, or if you sell a brokered CD on the secondary market for less than you paid.

How much does a $10,000 CD earn at 4.94% APY?

A $10,000 deposit in a 12-month CD at 4.94% APY earns roughly $494 in interest over one year, before taxes. The exact amount depends on compounding frequency, but the APY standardizes the comparison.

Is a CD or a high-yield savings account better right now?

It depends on when you need the money. A CD locks a fixed rate for the term and usually pays more than a savings account, but you give up liquidity. High-yield savings accounts offer full access to your cash at variable rates that can change anytime. For an emergency fund, liquidity usually wins; for a known expense six to eighteen months out, a CD often makes sense.

Bask Bank

Bask Bank Bread Savings

Bread Savings Capital One Bank

Capital One Bank Colorado Federal Savings Bank

Colorado Federal Savings Bank E*TRADE

E*TRADE First National Bank of America

First National Bank of America Marcus by Goldman Sachs

Marcus by Goldman Sachs Popular Direct

Popular Direct